It's that time again, early in the new year, when we are speculating as to what 2023 may hold, in this case for the property part of the South African economy.

READ: A guide to securing commercial property financing for entrepreneurs

With the expectation of a renewed economic weakening, on the back of a global economic slowdown, recently rising interest rates, and major electricity supply problems, a broadly weaker property market in 2023 (compared with 2022) is anticipated. With consumer price inflation slowing, FNB believes that interest rates are near their peak, but the full impact of rate hikes has yet to be felt. The industrial property market is expected to remain the relative outperformer albeit with a slower year in that property class also anticipated.

The recently strengthening residential rental market may ''level out'', and 2023 is expected to be slower for residential development. The Western Cape, whose economy may be starting to benefit more noticeably from years of relatively sound regional management and superior attraction and retention of skilled labour, could be the outperforming regional property market in 2023.

Here are the key themes, or features, that we think will be worth looking out for:

1. A slower economic growth rate in 2023 could cause a renewed rise in the All Property Vacancy Rate.

The MSCI Bi-Annual All Commercial Property Vacancy Rate was on a broad multiyear rising trend, from a low of 4.2% as at the 1st half of 2016 to 9.5% by the 1st half of 2021. Then, a rebound in the economy in 2021, following the hard lockdown recession of 2020, led to some minor decline in this vacancy rate to 8.2% by the 1st half of 2022.

However, a renewed increase in economic pressure may once again place additional constraints on commercial space demand in 2023, in turn causing the national vacancy rate to resume the earlier rising trend this year.

FNB projects Real Gross Domestic Product (GDP), the measure of economy-wide production/output, to grow by a slower 1.2% in 2023, following an estimated 2.3% in 2022. This slower growth forecast is the expected result of a slower global economy impacting on SA's trade-related production for the rest of the world, the lagged impact of a recent series of interest rate hikes still to feed through, and with a key further recent source of pressure being an escalation in the level of Eskom electricity load shedding.

We expect one further 50 basis point interest rate hike at the January SARB MPC (Monetary Policy Committee) meeting late this month, bringing interest rates to their expected peak with prime rate reaching 11%. But, as mentioned, it takes some time for the full cooling effect of rate hiking to feed into the economic numbers.

READ: What to consider when buying or renting your business premises

2. The end of rising interest rates would ease one source of upward pressure on capitalization rates, but weaker property income prospects may sustain the slow upward drift in 2023.

While the expected end to interest rate hiking this month may serve to ease one source of upward pressure on property capitalization (cap) rates, another source of upward pressure may intensify, namely the expected weaker property income growth prospects.

Financial pressure on South Africa's commercial tenant population is expected to increase, driven by slower economic growth this year, and a higher average interest rate on debt compared to 2022. In addition, operating cost inflation faces upward pressure from the next severe electricity tariff hike recently approved, while many businesses may have to incur further costs to ensure a reliable electricity supply in the face of recent further deterioration in Eskom supply reliability.

In addition, from a decade low monthly average of 6.9% in May 2013, the monthly average Government long bond yield (10 years and longer) ended the year 2022 4.5 percentage points higher at an average of 11.38% for December. This broad rise in these longer-term interest rates has been a key influence on cap rates too, driven higher by a long term deterioration in Government finance, Government debt issues rising sharply over the past decade, and few noticeable improvements are expected in 2023 as slower economic growth likely constrains Government revenue growth.

We would therefore expect the continuation of the gradual multi-year upward drift in cap rates through 2023. During the multi-year commercial property valuations correction, which commenced around mid-last decade, the average regional shopping centre cap rate has risen from a 7.5% low in the 1st quarter of 2015 to 9.3% in the final quarter of 2022 (according to Rode and Associates data). Average prime industrial cap rate rose from 8.9% to 9.9% over the same period (Rode data), and National A-Grade de-centralised office cap rates from 9.3% in the 3rd quarter of 2015 to 11.3% by the end of 2022.

Capitalisation rates have thus drifted significantly higher since multi-year lows reached around 2015, and we don't yet expect a reversal of this broad trend.

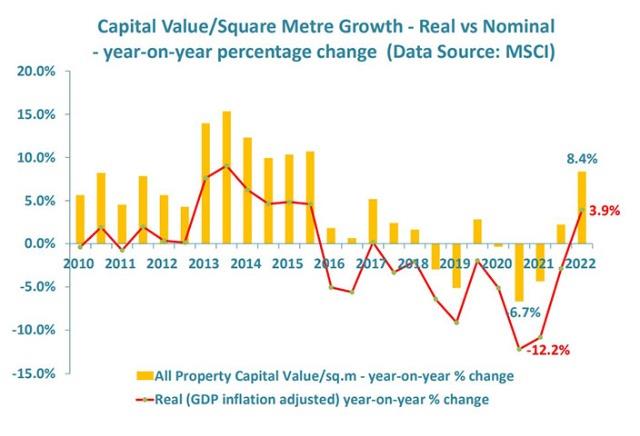

3. Average capital value per square metre of commercial property expected to shift back into slower nominal growth but "real" (inflation-adjusted) decline.

MSCI data for the 1st half of 2022 showed the 1st noticeable ''real'' (GDP inflation-adjusted) year-on-year growth rate in the All Property Capital Value/Square Metre since the 2nd half of 2015. In actual value terms, there have been quite a few semesters with low positive single-digit actual growth in average capital value, but they have rarely kept pace with general economy-wide inflation since 2015, therefore translating into a correction in average commercial property values in real inflation-adjusted terms.

We do not yet think that the long-term correction is over, given the sluggish state of long term economic growth in South Africa, with its myriad of mounting structural constraints. Rather, we believe that the positive real growth rate of 3.9% (GDP inflation-adjusted), and 8.4% year-on-year growth in actual value terms, was likely the result of valuations coming off a very low base caused by the severe 2020 lockdown-related recession drop, valuations merely ''normalizing'' partially as the economy opened up to business once more.

Given the abovementioned renewed sources of economic pressure, i.e. economic slowdown and rising interest rates since late-2021, it is expected that capital value growth will once more slow back into single-digit territory in 2023, not keeping pace with general inflation, and the real long term valuations correction will once again resume. How far are we into the multi-year correction in real property values? Compared with the 1st half of 2018 high, average capital value per square metre was only -2% lower as at the 1st half of 2022, having made up a significant portion of its lockdown drop, according to MSCI data.

4. All 3 major commercial property markets are expected to be weaker in 2023, compared to 2022, with Office remaining the underperformer, Industrial the relative outperformer, and Retail somewhere in the middle.

- The Office Market has many challenges

The office property class is expected to remain the underperformer of the 3 major commercial property classes in 2023, with its already high average national vacancy rate of 18.5% (according to MSCI data) as at the 1st half of 2022 expected to rise further.

This major property class is expected to see its national average vacancy rate continue to rise in 2023, with little to drive any significant growth in demand for space in the near term. Some companies are believed to be gradually revising their office space needs downwards. Much has been made of the work from home (WFH) surge, and this has been a key dampener of demand for office space.

Following the end of lockdowns, and the ''normalization'' of economic activity, A portion of the office work force has returned to their offices. However, we believe that the level of office attendance does not appear to have gone back to the same levels as before the lockdowns, and as technology continues to improve, so the multi-decade trend towards greater remote work levels will likely resume (following the initial ''back to the office'' move after the lockdown spike).

People also often overlook 2 other sources of pressure on demand for office space. The first is the normal ''weak economy'' effect, which caused a major drop in employment numbers in the office-bound sectors of the economy. This means that, even without any increase in remote work, there are less employees in these services sectors, which would normally imply less office space needed. Employment numbers in the Finance, Real Estate and Business Services Sector, a key driver of office space demand, was still -3.7% below the 1st quarter of 2020 level (just prior to lockdown) as at the 3rd quarter of 2022.

In addition, the trend towards improved utilisation of desk space seems to have picked up, with ''hotelling'' of desk space increasing in popularity. ''Hotelling'' refers to a desk booking system, something Firstrand has also implemented, meaning that employees either book a desk for a day or they don't have one. Gone are the days' therefore, when every employee had a desk reserved for themselves, meaning a large portion of desks standing empty much of the time.

This sharing of desk space is likely to further reduce the need for office space. Social distancing measures in the office, which required more spaced-out desk arrangement, are also largely a thing of the past. These above-mentioned factors are expected to leave the Office Market under pressure in 2022 with its average vacancy rate rising further, little new office development and the drive to repurpose a portion of this market to residential properties continuing.

- Retail has a financially pressured consumer to deal with.

The retail property environment, too, is expected to be more challenging in 2023, compared to 2022. While consumer price inflation may gradually slow, eating less into household disposable income growth as the year goes on, the average interest rate on household debt is projected to be significantly higher in 2023 for the year as a whole, compared to 2022.

FNB anticipates a further 50 basis point rate hike in January, bringing the current rate hiking cycle to an end, whereafter it expects only one 50 basis point reduction later in the year. This implies that the year will end on a prime rate of 10.5%, where it currently stands now. Slower economic growth in 2023 will also likely translate into slower employment growth, and real household sector disposable income growth is forecast to slow from a positive 0.8% in 2022 to a negative -0.2% in 2023.

- Industrial Property has the most going for it in 2023, but its main economic drivers are still under pressure.

We expect the Industrial Property Market to remain the relative outperformer of the major commercial property classes. It is the most affordable of the 3 classes, and arguably the most adaptable, and this puts it at a relative advantage when the economy is under financial pressure, although it can't entirely avoid the current economic pressures.

In addition, it appears set to benefit relatively-speaking in the coming years from increased online retail focus. However, in 2022 our FNB Property Broker Surveys did point to signs that demand for this property class may have also been peaking for the time being, rising interest rates and a weakening economy also taking its toll here. Real seasonally-adjusted Manufacturing Gross Value Added (GVA), a key driver of industrial space demand, was still -9.3% below its end-2018 high, and had only shown growth of 0.3% year-on-year for the 1st 3 quarters of 2022.

Economy-wide inventory levels have also declined significantly in recent years, so the traditional economic fundamentals related to industrial property are not overly strong. Nevertheless, the FNB Commercial Property Broker Surveys of recent quarters have still shown the Industrial Market to indeed have been the strongest one of the 3 markets through 2022, and the only one of the 3 markets where brokers perceive the average vacancy rate to have significantly declined.

READ: Here's where the smart money is investing in commercial real estate

5. Residential Rental Market may be peaking in 2023.

The Residential Rental Market may be in the process of ''peaking'', and may level out in 2023. TPN data had seen a reasonable recovery (decline) in the national residential vacancy rate estimate from just after the 2020 lockdown to mid-2021. And the CPI for actual residential rentals saw its year-on-year rate of inflation go from a lowly +0.61% as at March 2021 to 2.82% by the September 2022 CPI survey. TPN also reported a significant recovery in tenant payment performance following the 2020 lockdown dip.

However, while rising interest rates can initially strengthen a rental market, as aspirant home buyers delay purchases and rent for longer in some cases, ultimately the rising interest rates and a slowing economy can begin to exert financial pressure on rental tenants. After a very significant 350 basis points' worth of interest rate hikes to date, and a further 50 basis points still expected, such renewed pressure may have begun, and the December CPI rental survey actually showed a slightly slower rental inflation rate of 2.5% year-on-year (from 2.82% in the prior survey). This was due to a slowing in the rental inflation rates on houses and townhouses, with only the smallest and most affordable flats component still showing a further acceleration in inflation.

Therefore, we believe it possible that the mild post-lockdown residential rental market recovery may have run its course, therefore, and this market may ''level out'' in 2023 as interest rates hit their expected peak and then start to decline mildly late in the year.

6. Residential development market to have a slower 2023.

The residential rental market is expected to slow in 2023, after a reasonable pick up following the 2020 interest rate cuts and the end of hard lockdowns in that year. Higher interest rates have gone some way to cooling home buyer demand, and with a lag this normally translates into slower newly developed home demand as the existing home market becomes better supplied.

Residential building plans passed, a lead indicator of building activity to come, saw a -6.4% year-on-year decline in the 3rd quarter of 2022, after a bout of solid positive growth in prior quarters. It therefore appears likely that building planning has already begun to slow in response to interest rate hiking, and this points to a slower 2023 on the new residential building front. Only late in 2023, should FNB's forecast for the start of mild interest rate cutting prove true, could we see renewed strengthening in home buying demand followed by newly built home demand, but that would more likely translate 5 into renewed positive growth in residential building planning only in 2024.

7. Western Cape Region expected to be the outperformer economically and property-wise, as "semi-grants" continue to flock to those parts.

With regard to major regions' property market performance, we believe that the Western Cape province could be the likely outperformer in 2023. For some years we have believed that the Western Cape has a superior ability to attract ''semi-grant skills and purchasing power'', crucial for economic growth.

The province has been the most popular net middle-to-higher income group ''semigration'' (semigrant inflows minus outflows) destination for many years now, due to the perception of the province as having a great lifestyle coupled to significant economic opportunity. It has also been seen to be a region where provincial and local government is relatively well-run, translating into relatively good services and infrastructure provided to the more skilled part of the labour force and middle to higher income retirees.

These are groups whose purchasing power and skills are key to driving a regional economy. And as time has passed, communication and information technology has enabled businesses and individuals to be more removed from the major economic hub of Gauteng. In 2021, the unrest and looting in KZN and Gauteng may have further enhanced the relative appeal of living and doing business in the Western Cape, a province that largely escaped that event. In addition, the City of Cape Town is the only one of the major 6 metros that emerged from the 2021 local government elections with its ruling party having a clear majority, and thus free of the uncertainty of coalition politics.

8. Finally, electricity will be a key property theme in 2023, perhaps even more so than ever before.

Finally, electricity supply and cost appears set to be a major property market theme in 2023. We have already alluded to the recently heightened state of load shedding by Eskom having an indirect impact on the property market's performance via its negative impact on economic growth and resultant demand for commercial space. But the problem goes far further than that.

There is also a direct operating cost impact on property owners and tenants. NERSA (National Energy Regulator) recently approved a further sharp Eskom tariff high of 18.65%, which will have a significant impact on what is a major operating cost item. But the cost implications likely go far further. As Eskom's electricity supply reliability deteriorates, we have recently seen load shedding hit new record highs. This likely requires major investments by property players to reduce dependence on Eskom's grid supply further, at likely great cost.

Of all the expected property-related themes mentioned above, it seems likely that the state electricity supply will attract the most attention by far in 2023.